A combination of style, ‘coolness’, driving pleasure and sheer personal preference. If you have a better list or just one model you want to add the list, let me know.

Lotus Elan

The original. Copied by so many since its launch in 1964. But I’m not looking at the original 1500 model, my eyes are focused on the 1971 final rendition Sprint version.

Still using the original Ford engine this little rocket only produced 125bhp. But could get to 60mph in around 6.5 seconds. Mainly due to its meagre weight of 1,500lbs.

Not a car for the American market, where the Corvette of the day (C2) dwarfed it with power and top speed. But it did weighed twice as much at more than 3,300lbs. The little Elan was near uncatchable on a twisty road.

The list is the personal preference of our Director, Guy Winter. A car fanatic since the 1960’s, he eats’, sleeps and dreams everything Motor Trade. For the past 25 years he has worked for Cymark providing digital and telephone marketing support for individual retailers, groups and manufacturers alike.

If you want to stay on top of the latest Motor Trade chat either subscribe to this blog or find Guy on Linkedin.

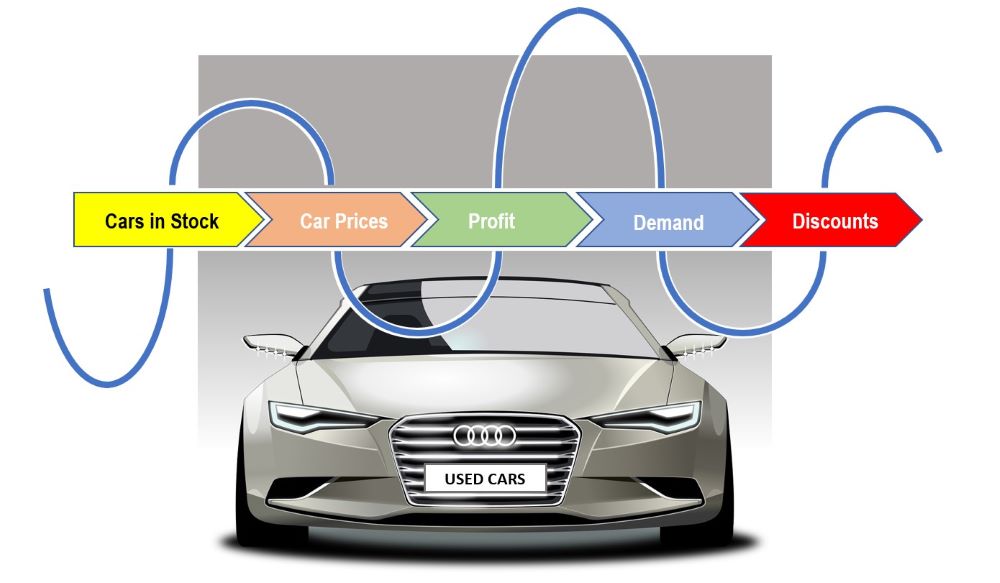

In the car world, I think, we would like to know what stock we should be carrying into Qtr1.

In addition to retailers reducing the levels of very expensive stock on the books we also have the dilemma of petrol, diesel or electric and hybrid.

The #BEV and #PHEV models have been looking very unattractive, mainly because retailers were blowing thousands of pounds on the part exchanges they took in. You don’t want to be caught with a £4,000 loss per car.

And the customers know this. It took a few months, but buyers cottoned on to the fact that the electric cars they could smugly show the neighbours are now, potentially, a bit of a disaster area for residual values. At least they purchased the car on PCP with fixed balloon payments.

So no problem them. Well, someone has got to pay and I’m sure the finance houses will keep their rates high long enough to clear any debt. Which might slow the start of 2024.

So what about January and Quarter 1?

We are urging retailers to get their plans in early, our call centre is filling up with fast start events from retailers looking to get 2024 off to a flying start. The hope is that manufacturers come on board with continued deposit contribution offers.

If you have pencilled in either new or used car events for January and February give us a call so we can reserve your campaign a calling slot. Don’t leave it too late like many dealerships did in 2023.

Following on from my earlier article, ‘The Rise and Fall of Used Car Sales’ , I’ve been doing a little digging while on my business trip to America.

You may remember, I questioned the difference in the conversion rates sales executives were seeing in America compared with the UK. American trade articles and websites were telling me that 50%-60% of customer enquiries are buying, continuing to be the norm, and everything was rolling along GREAT.

To see for myself, if it really was that much better than the UK – where 20%-25% is the accepted norm – I tried a little experiment.

The mystery shop.

To call it a mystery shop would be misleading. I was actually looking to buy an SUV, I just visited a lot more dealerships than I would normally.

Out of all of them, only 12.5% actually asked me for my contact details. That’s one in 8.

Now the US advertised conversion rate percentage makes sense. If a sales exec is only going to record the name of a customer if they are waving a credit card under their nose, then a 50%-60% conversion makes sense.

But what about all those ‘potential’ customers? ‘Me’ for example. I’m still sat here looking to buy a mid-range SUV, and the phone has only rang once.

The only dealership to ask for my contact number and email address AND actually send me something immediately and follow that up by telephone 24hrs later was the Kia Dealership in St Petersburg.

I will say, all of the staff, in all of the dealerships – with the noticeable exception of BMW – were very polite and professional. They provided all of the information I needed and it was a pleasurable experience.

But I have no idea why the other, 7/8, dealerships didn’t ask for my number allowing them to call me.

Maybe its fear around GDPR and data protection in America. But as I had walked into the showroom, sat in their cars and said ‘I WANT TO BUY A CAR’, I think that covers future contact under legitimate interest.

So it looks like the USA or rather 87.5% of US car dealerships, actually have a 20% conversion rate. They just, collectively, dropped the ball by not asking all of the customers that walk through the door for their telephone numbers.

I was surprised. Disappointed. But surprised for sure.

The fluctuation in both demand and used car prices continues its meteoric rise and ‘off a cliff’ fall though Qtr4.

Looking back through various trade articles issued in 2023, this is certainly nothing new. It’s just that previously there was quite an overlap between demand, availability and profit per unit that retailers were able to hold onto.

But is this a return to Qtr4 figures of old?

Mixed opinions, 2/3 of retailers are saying this is what we have always experienced and only a 1/3 saying the problems are due to retailers are now expecting car sales profits to continue month in, month out through the whole year.

Its not surprising that Manheim reported that conversion rates were falling, the ratio dropping a 1/5th on the same period in 2019.

We can however, report that our retailers are seeing a healthy increase in enquiry levels – hugely in the case of used cars from monthly figures over the past 4 years.

And, their conversion rates are holding up strong, but then they are using our enquiry follow-up / lost sale programmes so it is a little difficult to predict how other retailers are fairing.

If you’re conversion rates are not what you’re expecting it then it might be worth trying a sample batch of calls with Cymark. At least you would get a true picture of what your customers are saying.

Back in the market, particularly the UK, the reluctance to take anything electrical in part exchange continues – unless you have an outlet for the car – as their prices continue to fall heavily week to week.

Traditionally stock of the expensive models has always been run down over the winter months, just so you didn’t have to write them down. I think that is still continuing, it’s just that the number of cars that now fall into that ‘expensive model’ category has risen so much.

“Don’t get caught with it”, still prevails.

US / UK Conversion rates.

I was interested, while here in America, that US retailers expect a 50%-60% conversion rate, while in the UK, 25% is the more generally accepted average. It does make me wonder if either the customers are a lot more switched on and margins are lower in the States or – which is my probable leaning – the UK retailers are much better at getting contact details for ‘any customer that enquired’.

All I can say is, out of all the car buying customers I know in America, very few have ever had a follow up call or DM piece relating to a similar car they enquired about 2 months ago (or 6 months or 2 years!).

If you want a little more information about conversion rates and how to keep them strong. Drop me a message below and subscribe to the blog or Cymark on social media.

I’m currently on my bi-annual work trip to America and wanted to bring you first hand news of current dealerships impression from this side of the Atlantic.

As in the UK, manufacturers are still hyping up the benefits of going electric, but US retailers are confirming that the buying public just isn’t behind it.

First adopters in urban homes, where location permits, are running two ‘main’ cars having an extra model on the driveway, a petrol for the longer trips and an electric for the commute.

A huge difference in incentive – Over here there seems to be a real mixed bag covering what drivers can get charged for –

Purchase Tax on the car varies state to state and can be as little as 0% right up to 7% of the cars value. Obviously if you live near one of those 0% state borders, it is probably worth making a weekend of it and driving some distance to pick up the car.

Emission Tax? well, no. Not really. There is a gas guzzler tax aimed at the economy of the car itself but not the amount of CO2 that comes out. This is apparently changing in the future, but many owners are sceptical.

MOT. Again, it varies State to State, but even the states that do have a vehicle test, that test is mainly limited to the time the car is sold from a retailer and isn’t comparable to the UK test. For the rest of the States it is definitely buyer beware.

As one owner put it. “Why do I need to buy electric if no one is checking? Sure, I want to help save the planet, but not at that cost.”

This is echoing the message we are hearing back in the UK through our enquiry follow up calls.

The calls are designed to improve the conversion rate of all the enquiries that land at a retailer, which it most certainly does, but the – ‘reason for not purchasing your car’ – response is very enlightening.

The number of customers that don’t really like the hands off, on-line only option is very high in the UK, outside of those customers that will always choose the latest thing, and its the same in America. A lot of disbelief that it will work at all, despite Hyundai ramping up their plans to sell new cars through Amazon.

More and more customers are waiting to see what the future is bringing, some very cheap Asian cars, hydrogen or yet another change in the rules. If Ford America can pull back from building a new electric battery factory in Europe, “there must be something in it”, is their reasoning.

The resale value of EV’s after 7 years is worrying many customers, driving down the used car value and PX prices. Some of the depreciation reported is frightening potential buyers.

One both sides of the pond. We really need to keep an eye on what customers are thinking. Sure, to sell more cars, but also to get a better idea of what our customers are really thinking.

Some good news for a change. The enquiries from Qtr2 and Qtr3, that didn’t buy, are still there.

As the old saying goes – “Deal or Dead”, well they didn’t die. They were just asleep and now they are buying.

We just need to make sure it is from you!

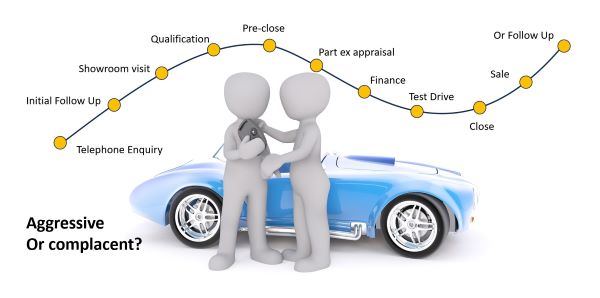

Having made enquiry and lost sale follow up calls for Motor Dealers for over 25 years we have a pretty good picture of what goes on in the showroom and in the sales exec’s mind.

“It was ages ago. If they still want to buy, they will come back to me.”

Which as we all know is complete rubbish.

We prefer the adage, “If you don’t ask, you don’t get”. Well that’s what we do, on your behalf so you don’t have to rely upon a disenchanted sales exec’ doing it.

AND THE GREAT NEWS.

Opportunities are flowing back into the showroom, not just from enquiries a month ago (25%) but from customers that didn’t buy during Qtr2 and Qtr3.

A number of retailers are using these older records much like a mini-event campaign, much lower numbers, but we can work through them. AND the deals are coming in.

Do you have stock you didn’t have in May or June?

Do you have a lower rate finance or contribution support from your brand?

Then now is the time to contact those outstanding customers.

If you want to make sure it happens give Cymark a call or have a look on the website, or the Blog pages for similar updates. Its worth a look –

Who remembers the 1970’s ? And I don’t mean the weird music and dress sense. I’m talking about the motor trade for both cars and motorbikes.

In the UK, we were proud of our heritage with motor bikes. We built the best. Ok, they were a bit long in the tooth and you didn’t get much. But it was all about image. And no foreign manufacturers from the East could beat that.

But history proved us wrong. We were slow to compete, couldn’t offer the same value for money and, basically, over the next 10 years the British motor cycle industry died.

Has the European Motor Trade got it’s head in the sand?

Have they forgotten the lessons from the British past?

The Europeans make some bloody good cars. Not just the German models, but the British, Swedish and French as well.

But the Chinese are coming.

How long will the European motor industry last if the Chinese arrive with fully electric models from £10,000? It would have to be an amazing European car that could complete with that while costing £40,000.

Remember the buying public. The early adopters rushed towards the latest European Tesla copies, sure they were better made. But you paid a pretty price. Not all drivers will do that.

So, to compete with the Chinese, will Mercedes knock 20% off the price of their cars? Not if they want a stock holders revolt they won’t.

So where does that leave my colleagues in the UK motor trade. The dealers? I expect that a high percentage will move to welcome the likes of BYD and Geely to UK shores and add Chinese franchises to their existing showrooms or replace existing brands completely. If you can’t beat them join them. Do we have any alternative?

The classic Alfa Romeo GTA Corse ages into the Totem GT-electric.

The 1962 Alfa GTA Corse was a classic the moment it was conceived. To be fair, even the picture doesn’t do it justice. In real life the car is tiny. Small but perfectly proportioned.

And today you can get a modern rendering of that car. Watch the video below of the fantastic Totem GT-electric. Performance is staggering. But, so is the noise. Totem have manage to maintain 60’s style with a truly modern build quality and safety features.

Given that the modern version uses original body panels (sourced by Totem) but combines them with the very latest in electric battery and drive train technology you can see why are lucky few are queuing up to be owners in the 21st Century.

The video is worth watching, so are the links on the companies website (below) they even include a ICE engine sound that is linked to the output of the car. It sounds like a highly strung Italian racing engine is pulling you along.

Like marketing in general. Totem have focused on something that works, something that attracts the buyers and decided to ‘do it again’.

There is no age limit on a good design, be that a motor car, a piece of artwork or an advertising campaign.

If it worked once. It will work again.

In the Motor Trade we routinely run ‘Man from the Bank’, ‘Man from the Factory’, ‘VIP’ style events. Why? because they work.

Cymark is in the fortunate position in being able to provide a telesales and enquiry follow up service that works. A process that has been working since 1995.

Unfortunately not fortunate enough to own either a GTA Corse or a new GT-electric.

Since Q4 2022 dealership stock have risen back towards pre-Covid levels. In some cases, too much stock. But getting back to normal is not just about stock levels. It’s about attitude.

Over the last 6 months, through our lost sale follow-up calls, we have seen a continuation of the ‘reason for lost sale’ that became prevalent when we had limited stock. Namely – “We didn’t have exactly what they wanted, so they bought one elsewhere”.

Speaking to Sales Managers this has not been the whole truth. Quite often we get – ‘bloody hell, we have two of those!’.

The strong sales managers, before 2020, always seemed to know which people in the team were the closers, the working sales exec’s you could rely upon to talk the customer into the car you had. It might not have been the right colour, or the right spec, but – “Today Mr Customer, this is the right car for you.”

Have we been developing teams of order takers? It has been a growing issue for perhaps the past 10 years, but the pandemic brought it on in waves.

True, when the only cars to sell are new cars, cars that aren’t in stock and aren’t available to demonstrate, we built some very good teams of order takers. Explaining the pro’s and con’s of a vehicle that, as yet, doesn’t exist is not always easy.

But has it gone too far?

Our ‘Reason for Lost Sale’ analysis is showing more and more that the real reason your customer decided to buying elsewhere, wasn’t price or availability. They just weren’t closed.

Thankfully our calls are still showing that roughly 55% of customers still haven’t bought any car a month after they initially enquired. Out of those half again are actively looking for your brand now. Today.

So all is not lost.

You just have to know which ones to chase. Which is where Cymark comes in.

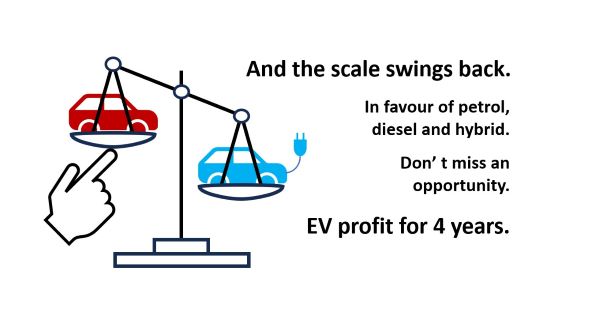

Do you need to close as many of those EV opportunities as possible before the latest EV reports reaches the mainstream motoring press?

Just this week, Bloomberg New Energy Finance (BNEF) answered a simple question, “When will electric cars be cheaper than ICE models?”. We aren’t 100% sure who asked the question but their response was interesting.

BNEF : “Well if you count the whole life costs of the car, you could say that is now. But, looking at manufacturing, we expect EV’s to be just 10% more expensive than their equivalent petrol engine model by 2027.”

Again, more great news for the buying public. At last the future of motoring comes back into the reach of so many small car buyers.

But TODAY, you need to make the most of all those EV enquiries. What if they dry up, waiting for these new 10% cars to arrive.

If Bloomberg are to be believed, and why not they are one of the largest financial institutions in America, then would you pay today, what is roughly a 40% over charge for some models, or would you buy something short term and wait it out.

Sure, there are some exceptions. The new Volvo EX30, when it arrives will be just £34k, only slightly smaller than the existing XC40, but starting price is exactly the same.

A bit like shrinkage in the supermarket, maybe that 10% was the packaging size.

If more manufacturers follow this Swedish lead, then perhaps the 10% models will be here sooner rather than later. However, looking at the other prestige models, the current line up’s all seem to be focused on the more expensive models.

We can only wait.

If you have rising manufacturers targets, that include EV sales you need to convert as many of those EV enquiries as possible with different enquiry management programmes like Cymarks Lost Sale and Enquiry Follow-Up programmes, both improve conversion rates.